Taxes

In 2012, subsidies for the transport sector contributed €28.6 billion to harmful impacts on the environment. A large portion of the existing subsidies, around €12 billion, is attributable to air transport. The subsidies consist of missing value added and kerosene taxes as well as ticket taxes that are too low. This distorts competition to the detriment of rail and other more environmentally-friendly modes of transport.

What about competition and infrastructure?

The airline industry’s argument against higher taxation is that companies have high costs elsewhere, e.g. airport charges and air traffic control. In addition, higher taxes would lead to competition distortions in international aviation; in addition, other modes of transport are subsidized. The aviation industry also claims to be the only mode of transport to entirely finance its own infrastructure costs. Rail travel is also cheaper than air travel in most cases.

An analysis conducted by Deutsche Welle (DW) comes to different conclusions. Especially on routes covered by low-cost airlines, a flight is cheaper than a train ride. However, the reduction in VAT for rail travel to the rate of 7% in 2019 should make domestic rail travel in Germany more financially attractive compared with air travel.

Moreover, the cost of airline tickets is in no way commensurate with the environmental impact of air travel. The complete financing of infrastructure by aviation also does not stand up to closer scrutiny: subsidies for regional airports and the financial disaster surrounding the construction of the new BER airport in Berlin are definitely a burden on the public purse. Taxes are also levied for other reasons, e.g. to finance education or social services and to put together rescue packages in times of crisis. Aviation also benefits from all this. Ultimately, taxes can also develop a steering role: the energy tax, for example, leads to a higher incentive for energy efficiency.

Closer to the desired effect

There is even the political will in the EU for higher taxation of air travel: in November 2019, the finance ministers of Belgium, Bulgaria, Denmark, France, Germany, Italy, Luxembourg, Sweden and the Netherlands expressed their support for an EU initiative to tax air travel. 72% of EU citizens also support a carbon tax on air travel. Nevertheless, from a climate protection perspective, current regulation is unfortunately far from what would be desirable.

Energy taxes

What is the current regime for energy taxes?

The energy tax is an excise duty that is currently applied on various fuels. Minimum tax rates are set at the European level, but Member States are allowed to impose higher tax rates. Aviation fuel for commercial operations is exempt from energy tax under the EU’s Energy Tax Directive 2003/96/EC. However, under Article 14(2), Member States have the option to remove this exemption for flights within the EU and for domestic flights. The minimum rate for EU energy taxes is 33 cents per litre of kerosene. For Germany, the taxes are set in the Energy Tax Act: For kerosene, the minimum rate here is 65 cents per litre, which is identical to the rate for petrol consumption in road transport.

Tax exemptions on national, European and international levels

At present, however, not a single EU Member State (including Germany) levies energy taxes on kerosene used on domestic flights. The subsidization of energy tax exemptions on commercial aviation amounts each year to approx. €27 billion across the EU and approx. €8 billion per year for Germany.

The tax exemption for aviation fuel is based on the agreement of the ICAO Convention signed in Chicago in 1944. However, the International Civil Aviation Organization ICAO does not prohibit the taxation of kerosene per se, but only in certain forms. For example, no kerosene may be taxed that is already on board an aircraft to be used on the onward international flight.

However, bilateral aviation agreements that regulate air traffic between two countries often mention tax exemption, such as the agreement between the EU and the USA (2007/339/EC). Such agreements are the basis for allowing aircraft to fly between the two countries, regulating ownership and control of airlines, and forming the basis for cooperation between countries with regard to safety and competition, for example. The notion of tax exemption dates back to the post-World War II era: the agreement not to levy kerosene taxes was widely used at that time to strengthen the expansion of the aviation industry and, in turn, international exchange.

Outside the EU, countries such as the U.S., Canada, Australia, Japan, Saudi Arabia, Thailand and Vietnam impose excise taxes on aviation fuel for national flights. Rates vary from €0.02 per litre in Australia to €0.70 per litre in Hong Kong.

What should the regulation of energy taxes look like?

It does not make sense for kerosene to be exempt from the energy tax. All fuels should be included.

From a climate protection perspective, a kerosene tax should be introduced as widely as possible, at least across the EU.

Since some Member States reject such a tax and a unanimous decision on taxes must be taken in the EU, it is currently difficult to implement such a tax across the board. However, it would be possible for some Member States to form an “alliance of the willing” and tax kerosene on flights covered by the alliance countries.

A kerosene tax should definitely be introduced on domestic flights. Legally, this would be possible without any restrictions. The Energy Tax Act theoretically provides for a levy of 65 cents per litre of kerosene, which would correspond to the tax on petrol. Kerosene refuelled in Germany for international flights could also be taxed. For this, bilateral agreements which currently prevent this would have to be amended. A kerosene tax would directly increase the cost of CO₂ emissions and thus take into account negative climate impacts. At the same time, as an excise tax, it could generate additional government revenue that could be used elsewhere for climate protection or other general purposes.

Furthermore, kerosene should be taxed in addition to being included in the EU Emissions Trading System. This is because the EU ETS only takes CO₂ emissions into account. An excise tax could additionally put a price on the other negative climate impacts of aviation.

Value added tax

What is the current regime for valued added tax?

No VAT is charged on international flights. Based on an average VAT rate of 19%, the EU-wide subsidies thus amount to around €30 billion per year. In Germany, the aviation sector thus receives subsidies of approx. €5 billion. Most Member States levy VAT on domestic flights, including Germany. Domestic flights account for only a small share of all flights in Germany. However, depending on the EU Member State, they account for between 6% and 27% of total flights.

According to the EU VAT Directive, no VAT should be levied in international air transport on the supply of fuel, the delivery, repair or maintenance of the aircraft themselves or their cargo. However, countries may levy VAT on airline tickets, as well as on fuel and airport or service charges. For example, the U.S. and Canada impose a sales or transport tax on flights between their countries and, in the case of the U.S., to Mexico. Mexico imposes a general transport tax of 4% on international flights.

How should value added taxes in aviation be regulated?

A value added tax is also urgently needed for international flights in order to reduce the subsidization of the most climate-damaging means of transport: the aeroplane.

An EU-wide VAT regime would be the most sensible solution to create a level playing field in the EU single market. This would require amending the EU VAT Directive, which sets the framework for national rules on VAT. A reform process of this directive has been underway since 2019. VAT could be levied in the country of departure for the entire flight. Such a change would be easy to implement and would have a large positive impact on the environment.

However, it is uncertain whether the EU Member States could agree on such a regulation. There are also major obstacles to the introduction of a value added tax for international aviation beyond the EU. The International Air Transport Association (IATA), for example, justifies the zero-percent VAT rate with the argument that international air transport takes place outside of any tax jurisdiction, thus enabling a level playing field for air traffic across national borders.

As long as these hurdles remain, it would make sense to raise the already existing ticket tax enough to compensate for the revenue lost due to the lack of VAT on cross-border flights.

Ticket taxes

What is the current regime for ticket taxes?

In Germany, ticket taxes – as well as air traffic taxes – are levied on commercial passenger flights departing from a domestic airport (the article of the tax is the legal transaction, e.g. the contract of carriage, which entitles the passenger to take off).

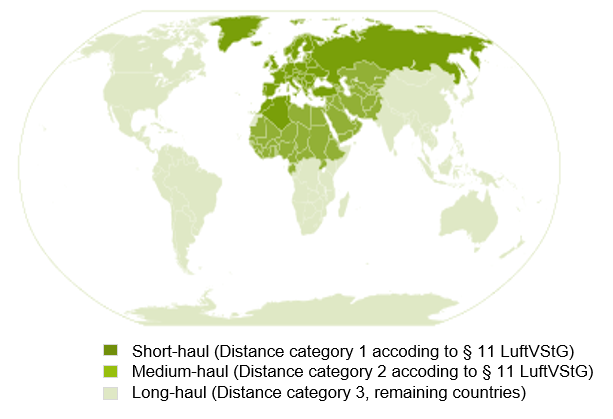

In Germany, ticket taxes are levied depending on the destination region. These are divided into three distance categories; the tax rates in 2020 range from €13.03 to €59.43 per departure in Germany. For domestic flights, the tax is paid for both the outbound and the return flight. These tax rates have been in effect since April 1, 2020 and were increased as part of the Climate Action Programme 2030. The tax applies to the entire flight from its departure in Germany to the destination airport, thus the distance category is not determined by the airports that serve only a stopover or transfer. Passengers who only change planes in Germany do not pay air traffic tax. Feeder flights within Germany are also not taxed separately; the tax rate for the destination applies. Children under the age of two and flights taken solely for official, military or medical purposes are not taxed.

The amount of the aviation tax is linked to the auction proceeds of the EU Emissions Trading System. The idea was that the combined total of aviation tax revenues and the auction income under the EU ETS would be one billion Euro per year, adjusted annually. With the new tax rates from April 2020, the sum has been increased to €1.75 billion.

Ticket taxes vary widely across Europe. In the UK, ticket taxes are comparatively high, averaging around €45 per passenger. Norway and Austria, on the other hand, have lower ticket taxes per passenger compared to Germany.

What should the ticket tax regime look like?

The ticket tax is intended to generate government revenue, but also to have an environmental effect. However, without VAT on international flights and without a kerosene tax, the ticket tax can only make a small contribution to reducing tax-based subsidization of air travel.

As long as no VAT is levied on international flights, the ticket tax should be raised so that it offsets taxes that are not levied.

An air transport tax should also be levied on the transport of freight. This is because current regulation only applies to passenger traffic.

It is particularly important that neighbouring countries coordinate their ticket tax systems. because here, too, it is difficult to find a Europe-wide solution directly. Germany should increase the tax for short-haul flights as a first step. Here, there is no significant risk that passengers will try to avoid the tax by choosing other flight routes. In other EU countries, furthermore, discussions about the ticket tax are also underway. France, for example, has increased its ticket tax in 2020, and the Netherlands plans to introduce a ticket tax in 2021.

Effects of ticket taxes

On domestic flights, an increased ticket tax could lead to a noticeable drop in demand in the short term, especially for journeys taken privately rather than professionally. This is because inexpensive domestic flights will become more expensive due to the double levy for outbound and return flights and the value-added tax charged. Since average tickets for domestic flights are in the middle price range, even for low-cost airlines, the impact of a higher ticket tax on the ticket price is not very high.

On international routes, the new rates of Germany’s Air Traffic Tax Act only lead to a relevant price increase for very low-priced tickets and thus to noticeable effects. For moderate to high ticket prices, the one-off drop in demand is less than 2%. Overall, it is estimated that a 10% higher price would lead to a decrease in demand by 9% to 11% in most EU countries. Moreover, higher ticket prices would not have a negative impact on jobs. Although jobs would be lost in the airline industry, the higher tax revenues would have a positive impact on the overall economy.

Another idea for regulating air transport more strongly would be progressive taxation: It could take into account the amount and distances of flights that an individual takes each year. The idea of a Frequent Flyer Levy (FFL) is to make each flight taken within a certain time period progressively more expensive, thus creating an incentive for fewer flights. An Air Miles Levy (AML), in contrast, would increasingly make the cost of the distance flown more expensive. Since low income groups fly less frequently and over shorter distances, they would not be affected by the price increases as much as high income groups. Nevertheless, these levies would need to be combined with other policy measures to sufficiently address environmental impacts of the aviation sector.

Links

-

CE Delft (2019): Taxes in the Field of Aviation and their impact.

-

EIB (2019): Weniger fliegen, weniger fahren: für Europa eine Option. Zweite Umfrage der EIB zum Klimawandel.

-

Transport & Environment (2019): Taxing aviation fuel in Europe, Study reveals ways around the regulatory hurdles, 2019.

-

Transport & Environment (2019): Domestic aviation fuel tax in the EU.

-

UBA (2016): Umweltschädliche Subventionen in Deutschland.

-

UBA (2019): Umweltschonender Luftverkehr, lokal-national-international (UBA Texte, 130/2019).

-

VCD (2012): VCD Bahntest 2012/2013.